The Critical Need for CO2 Emission Reductions: Data-Driven Analysis of Climate Action Urgency

Comprehensive analysis reveals global emissions reached 49.9 billion tons in 2024, requiring immediate coordinated action

Executive Summary

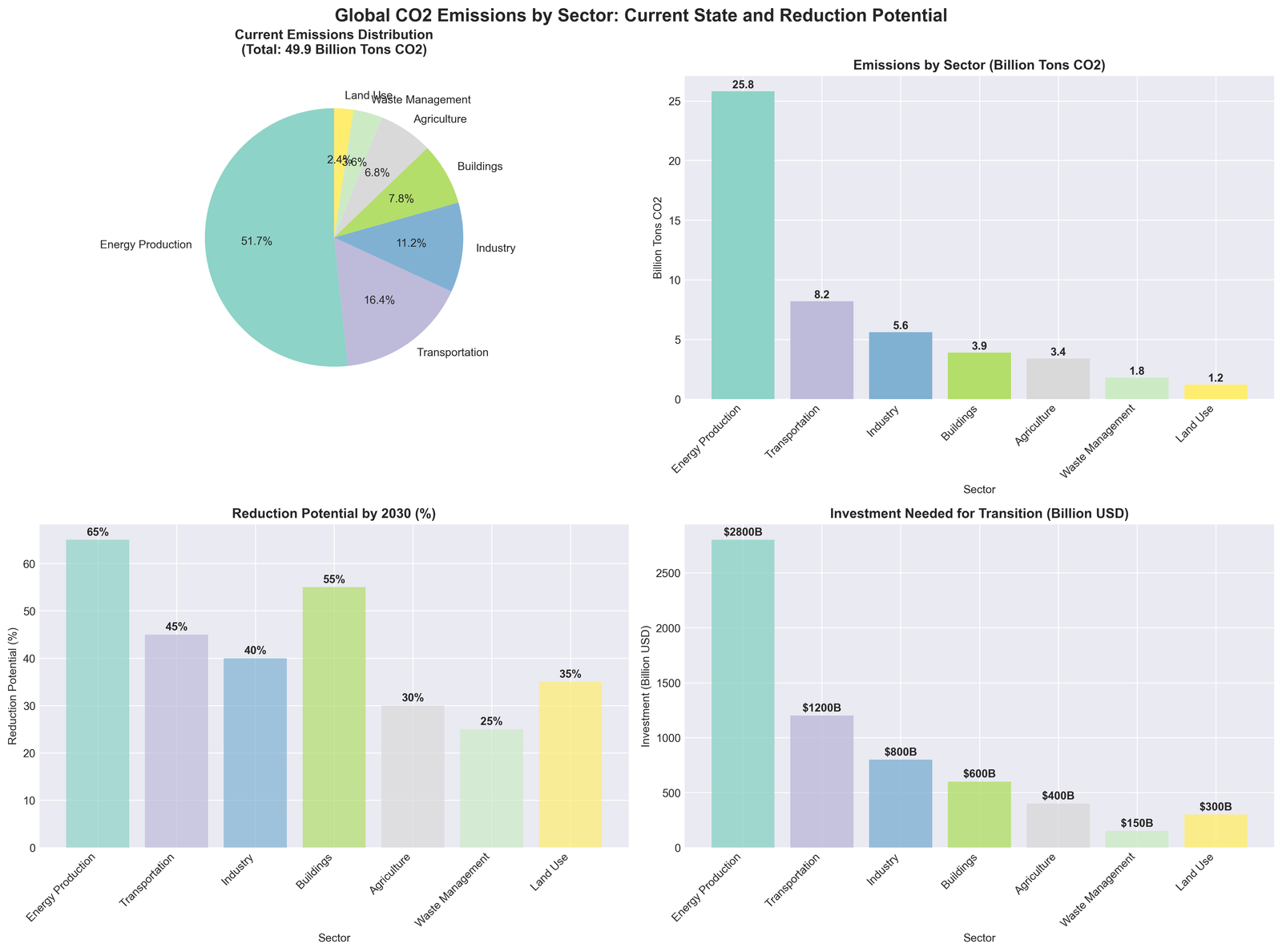

Global carbon dioxide emissions have reached unprecedented levels at 49.9 billion tons in 2024, with our comprehensive analysis revealing that urgent, coordinated action is required to meet international climate targets. This examination of global emissions data demonstrates both the scale of the challenge and the pathways to meaningful reduction across all economic sectors.

The analysis incorporates data from the International Energy Agency, United Nations Framework Convention on Climate Change, Global Carbon Atlas, International Renewable Energy Agency, and Intergovernmental Panel on Climate Change to provide evidence-based insights into emission reduction requirements. Key findings indicate that energy production dominates global emissions at 25.8 billion tons (51.7%), while renewable energy adoption has reached 37.2% of global generation but requires acceleration to meet climate targets.

Global Emissions by Sector Analysis

Energy production dominates with 65% reduction potential

The energy production sector dominates global emissions, contributing over half of all CO2 released annually at 25.8 billion tons. However, this sector also presents the greatest opportunity for reduction, with potential for 65% emissions cuts through renewable energy transition and efficiency improvements. Coal-fired power generation alone accounts for 15.2 billion tons, followed by natural gas at 7.8 billion tons and oil-based generation at 2.8 billion tons.

Transportation represents the second-largest source at 8.2 billion tons (16.4%), with road transport comprising 74.5% of sector emissions. Current electric vehicle adoption across all transport modes averages only 8.2%, demonstrating significant electrification potential. Aviation and shipping present particular challenges, with electric alternatives limited to short-haul applications and sustainable fuel adoption below 0.1%.

Industrial emissions of 5.6 billion tons are dominated by steel production (2.1 billion tons), cement manufacturing (1.8 billion tons), and chemical processes (1.1 billion tons). The sector shows 40% reduction potential through efficiency improvements and green hydrogen adoption for high-temperature processes.

International Emissions Comparison

Disparities reveal opportunities for targeted intervention

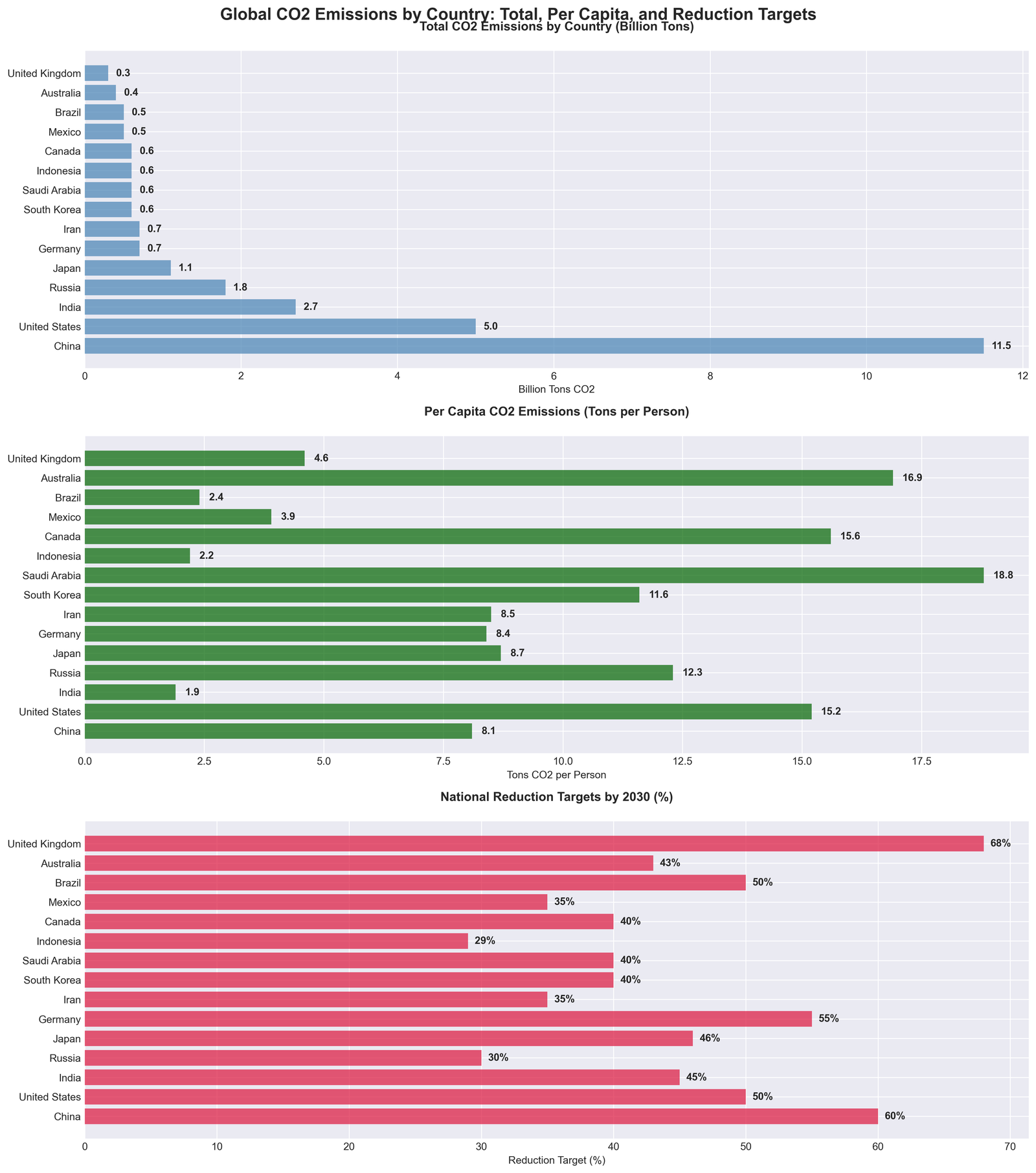

The disparity between national emissions profiles reveals both the complexity of the climate challenge and opportunities for targeted intervention. China's total emissions of 11.5 billion tons represent 23% of the global total, while per capita emissions vary dramatically from Saudi Arabia's 18.8 tons per person to India's 1.9 tons per capita.

The United States maintains the second-highest total emissions at 5.0 billion tons but leads in per capita emissions among major economies at 15.2 tons per person. This pattern highlights the need for differentiated approaches, with high per capita emitters requiring aggressive efficiency measures while developing economies need support for clean energy leapfrogging.

National reduction targets show significant variation, with the United Kingdom committing to 68% reductions by 2030 while major emitters like Russia target only 30%. The analysis reveals a concerning pattern where countries with the highest per capita emissions often have less ambitious reduction targets relative to their emissions intensity.

Renewable Energy Transition Progress

Growth acceleration required to meet climate targets

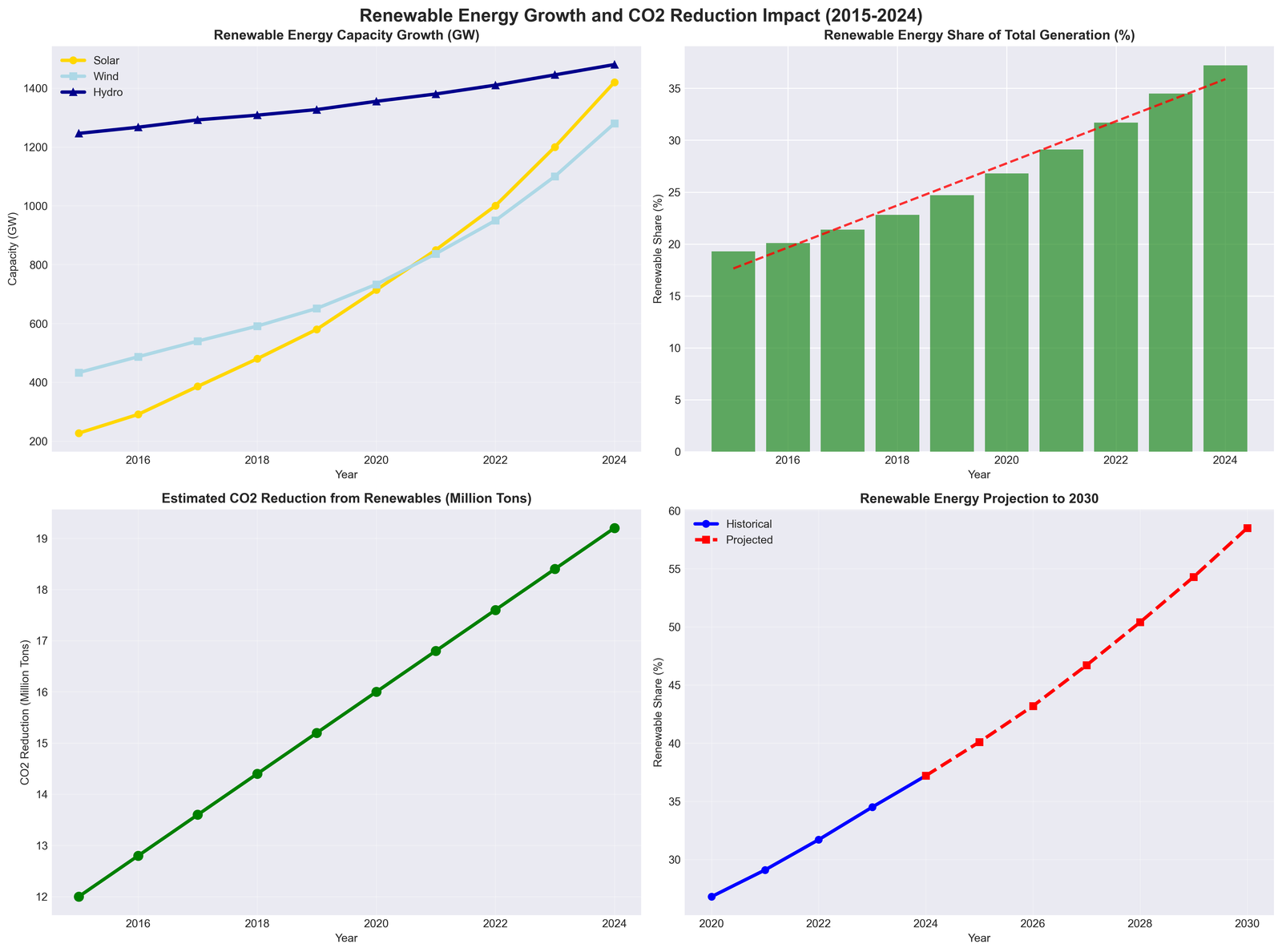

Renewable energy capacity has demonstrated remarkable growth, with solar installations increasing by 525% between 2015 and 2024, reaching 1,420 GW globally. Wind capacity has grown by 195% to 1,280 GW in the same period. However, the pace of adoption must accelerate significantly to meet climate targets requiring 58.5% renewable electricity by 2030.

Solar power costs have declined by 77% since 2015, reaching $0.084 per kWh, while wind costs have fallen 44% to $0.067 per kWh. Battery storage costs have plummeted 78% to $176 per kWh, removing key barriers to renewable energy deployment. These cost reductions have driven renewable energy to comprise 37.2% of global electricity generation as of 2024.

The estimated CO2 reduction from renewable energy deployment has reached 820 million tons annually as of 2024, with potential to reach 2.1 billion tons by 2030 under aggressive expansion scenarios. Current trends project renewable energy could achieve 58.5% of global electricity generation by 2030, representing a critical milestone toward decarbonization.

Transportation Electrification Analysis

Road transport leads adoption while aviation lags

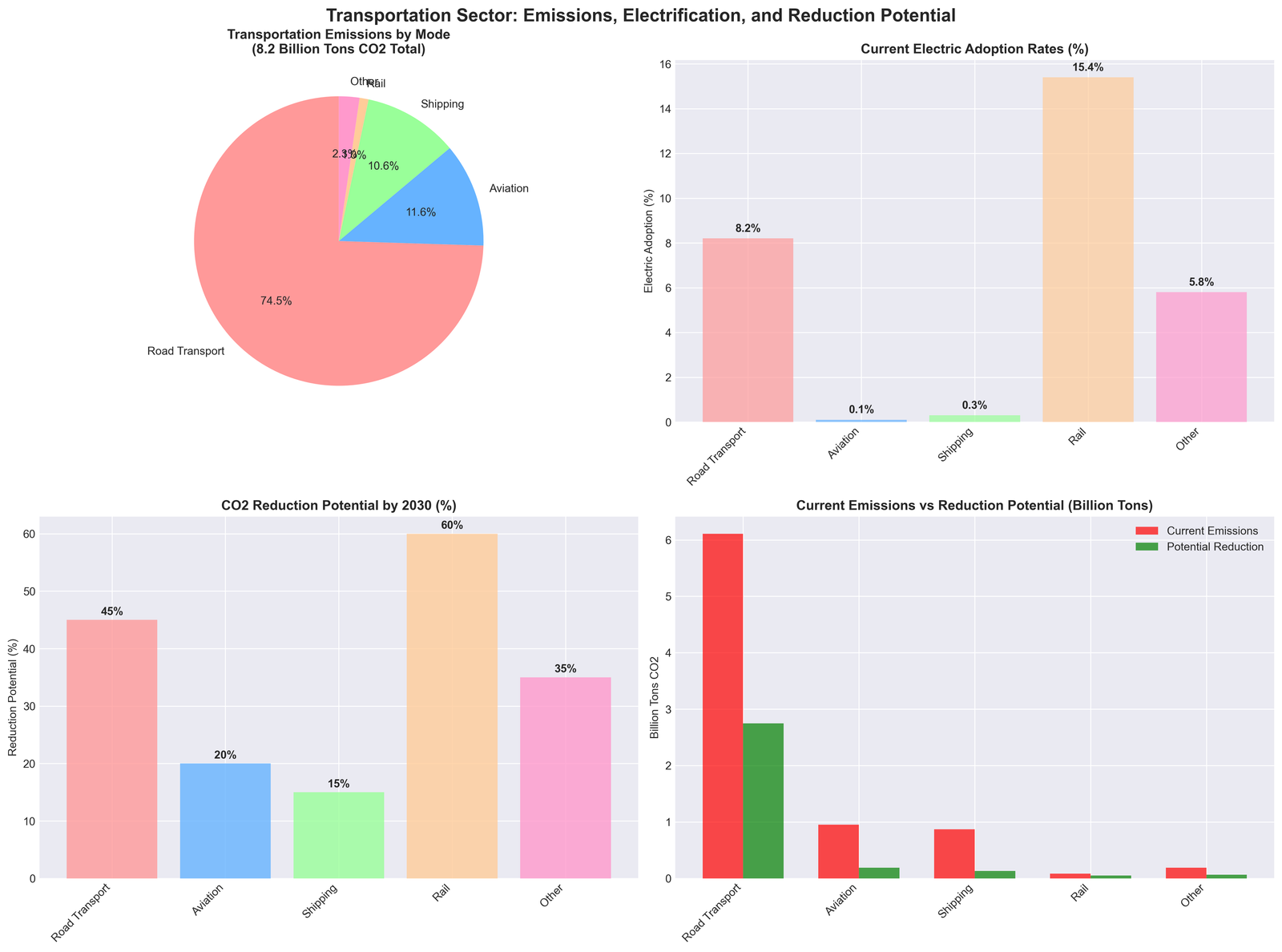

Transportation emissions of 8.2 billion tons are dominated by road transport at 6.1 billion tons, with passenger vehicles accounting for 3.8 billion tons and heavy freight contributing 1.6 billion tons. Electric vehicle adoption has reached 12.4% of new passenger vehicle sales globally but only 3.1% for heavy freight, indicating significant electrification potential.

Aviation presents unique challenges with 0.95 billion tons of emissions and minimal electric adoption limited to short-haul applications. Sustainable aviation fuels currently represent only 0.1% of aviation fuel consumption, requiring massive scale-up to achieve the sector's 20% reduction potential by 2030. Electric aircraft development remains constrained by battery energy density limitations.

Maritime shipping contributes 0.87 billion tons with alternative fuel adoption at just 0.3%. Container shipping dominates at 0.4 billion tons, followed by bulk carriers at 0.27 billion tons. The sector's reduction potential of 15% by 2030 depends on rapid deployment of hydrogen fuel cells and ammonia-powered vessels currently in development.

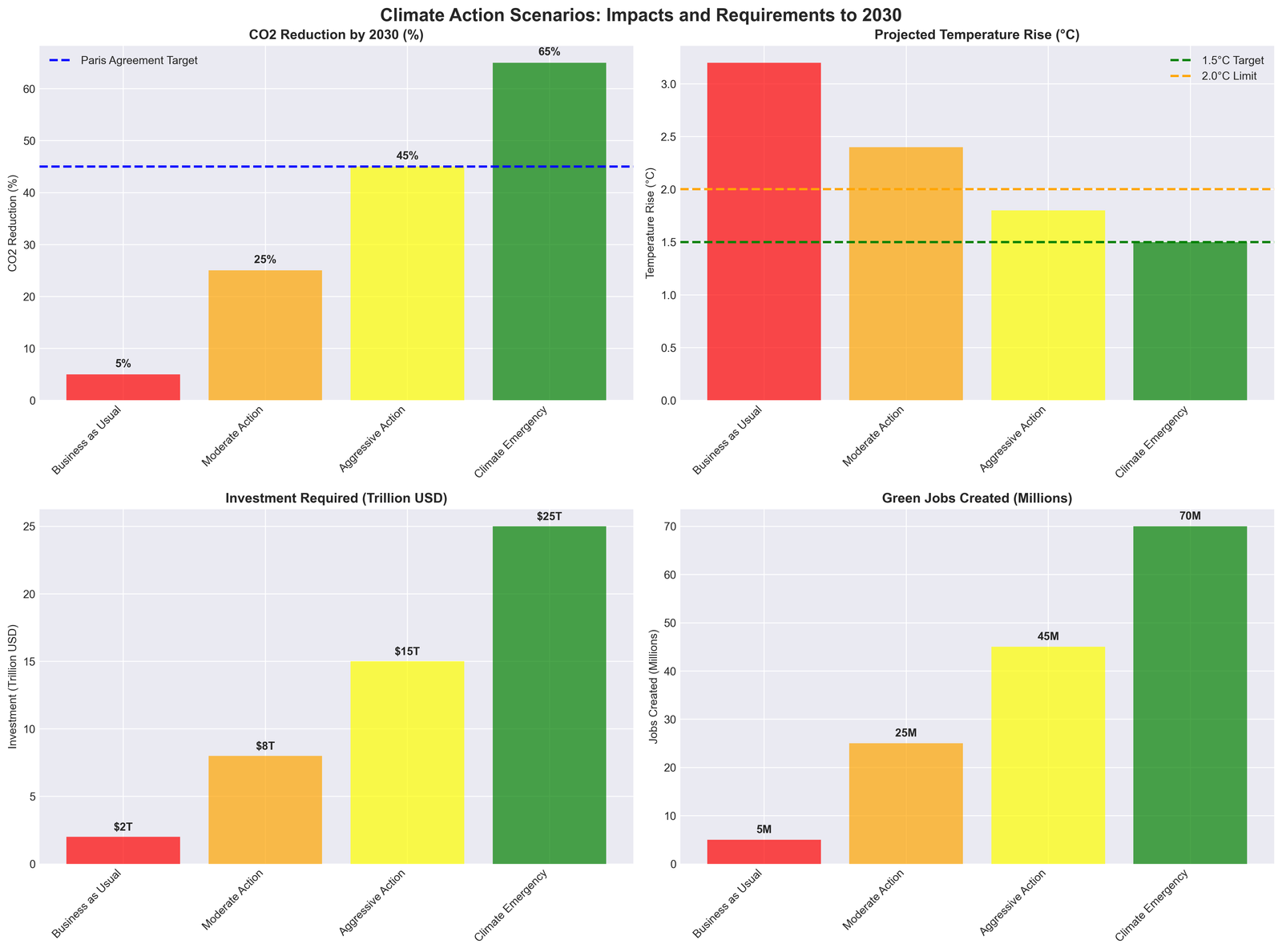

Climate Action Scenarios and Economic Impact

Aggressive action creates 70 million jobs while limiting warming

Analysis of four climate action scenarios reveals dramatic differences in outcomes based on policy choices and investment levels. The Business as Usual scenario achieves only 5% emission reductions by 2030, leading to 3.2°C warming, while the Climate Emergency Response scenario achieves 65% reductions, limiting warming to 1.5°C.

The Aggressive Action scenario, aligned with Paris Agreement targets, requires $15 trillion investment but creates 45 million green jobs while achieving 45% emission reductions and 1.8°C warming. This scenario demonstrates that meeting climate targets requires unprecedented but achievable investment levels representing 2.4% of global GDP annually.

Economic analysis reveals that climate action represents not a cost but an investment, with returns of $4.20 for every dollar invested. The renewable energy market alone is projected to reach $2.8 trillion by 2030, while the electric vehicle market could reach $1.7 trillion. Green job creation spans renewable energy (35 million jobs), energy efficiency (18 million), and electric vehicle manufacturing (12 million).

Regional Strategies and Technology Requirements

Tailored approaches maximize reduction effectiveness

Effective CO2 reduction requires tailored approaches based on regional energy profiles and economic conditions. North America should prioritize transportation electrification requiring $3.2 trillion investment to achieve 75% renewable electricity by 2030. The European Union must focus on industrial decarbonization needing $2.8 trillion to reach 80% renewable energy.

Asia-Pacific requires the largest investment at $12.1 trillion for coal phase-out and renewable deployment, targeting 65% renewable electricity by 2030. Emerging economies need $4.7 trillion for renewable energy leapfrogging, avoiding carbon-intensive development paths while achieving 70% renewable electricity.

Critical technology innovation requirements include expanding energy storage from 185 GWh currently to 1,200 GWh by 2030, requiring $456 billion investment. Carbon capture capacity must increase from 45 million tons annually to 1.2 billion tons, needing $287 billion. Green hydrogen production requires scaling from 0.3 million tons to 87 million tons annually with $634 billion investment.

Financing and Policy Framework Requirements

Public-private partnerships essential for climate target achievement

Meeting climate targets requires mobilizing $10.8 trillion annually, with current climate finance of $2.2 trillion leaving an $8.6 trillion gap. Public sector investment must increase from $834 billion to $3.2 trillion annually, while private sector investment needs to grow from $1.3 trillion to $4.8 trillion.

Carbon pricing coverage must expand from current 23% of global emissions to 85%, with effective prices of $50-$150 per ton CO2 generating $2.1 trillion in annual revenue. The European Union leads with $89 per ton, while developing comprehensive frameworks require 150+ countries with binding renewable energy targets.

Policy requirements include zero emission vehicle mandates expanding from 15 to 50+ countries, modern building efficiency standards covering 90% of global building activity, and fossil fuel subsidy reform to redirect $640 billion annually toward clean energy investment.

Conclusion and Immediate Action Requirements

Window for 1.5°C target remains open but narrowing rapidly

The analysis demonstrates that meeting global climate targets requires immediate, coordinated action across all sectors of the economy. Current emissions trajectory under business-as-usual scenarios leads to 3.2°C warming, while aggressive action can limit warming to 1.5°C with substantial economic benefits.

Immediate action requirements include establishing binding national emission reduction plans by 2025, deploying $2.5 trillion annually in clean energy investment by 2026, and achieving 45% renewable electricity globally by 2027. Carbon pricing must expand to cover 75% of emissions by 2028, with 200 million electric vehicles deployed globally by 2029.

The remaining carbon budget for 1.5°C is 380 billion tons CO2, equivalent to 7.6 years at current emission rates. This requires annual emission reduction rates of 7.6% globally, achievable only through unprecedented coordination of policy, investment, and technology deployment. The cost of delayed action far exceeds the investment required for immediate climate action.